Two kinds of banking licenses are granted by the Reserve Bank of India – Universal Bank Licence and Differentiated Bank Licence. Differentiated Banks (niche banks) are banks that serve the needs of a certain demographic segment of the population.

Small Finance Banks and Payment Banks are examples of differentiated banks in India. Custodian Banks and Wholesale and Long-Term Finance banks (WLTF) are newly proposed differentiated banks.

Differentiated Banks vs Universal Banks

Note: Subscribe to the ClearIAS YouTube Channel to learn more.

Differentiated banks are distinct from Universal Banks (Eg: Commercial Banks like SBI, HDFC, ICICI etc) as they are infused as niche segments. Niche banks typically target a specific market and tailor the bank’s operations to this target market’s preferences.

The differentiation could be on account of capital requirement, the scope of activities, or the area of operations. As such, they offer a limited range of services/products or functions under different regulatory dispensations.

Background of Small Finance Banks and Payment Banks

The concept of differentiated banks is not entirely new. In fact, and a sense, the Urban Co-Operative Banks (UCBs), the Primary Agricultural Credit Societies (PACS), the Regional Rural Banks (RRBs), and Local Area Banks (LABs) could be considered differentiated banks as they operate in localized areas.

However, the present concept of differentiated banks can be said to have been first discussed in 2007. Thereafter, the concept was once again discussed in the Paper “Banking Structure in India – The Way Forward”, brought out by the Reserve Bank in August 2013. RBI granted in-principle approvals to 11 entities for setting up payments banks (PBs) in August 2015 and 10 for Small Finance Bank (SFB) in September 2015.

Small Finance Banks (SFBs)

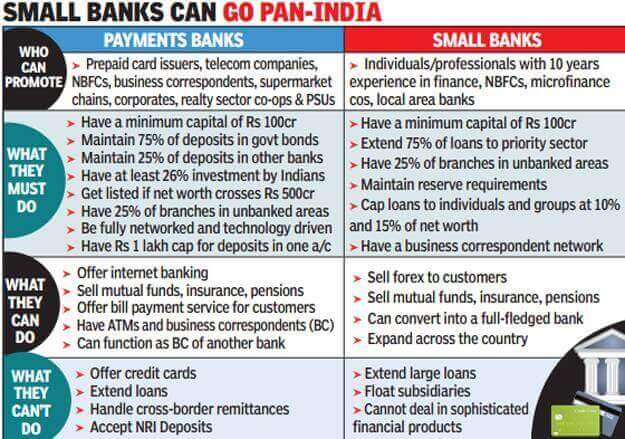

- They are niche banks that focus on and serve the needs of a certain demographic segment of the population.

- The objectives of setting up small finance banks will be to further financial inclusion by (1) the provision of savings vehicles (2) supply of credit to small business units; small and marginal farmers; micro and small industries; and other unorganised sector entities, through high technology-low cost operations.

- SFBs were recommended by the NachiketMor committee on financial inclusion.

Scope of activities of SFBs

- The small finance banks shall primarily undertake basic banking activities of acceptance of deposits and lending to unserved and underserved sections including small business units, small and marginal farmers, micro and small industries, and unorganized sector entities.

- There will not be any restrictions in the area of operations of small finance banks.

Criteria for setting up SFBs

- Individuals/professionals with 10 years of experience in finance, Non-Banking Financial Companies (NBFCs), microfinance companies, and local area banks are eligible to set up SFBs.

- The minimum paid-up equity capital for small finance banks shall be Rs. 100 crore.

- The promoter’s minimum initial contribution to the paid-up equity capital of such a small finance bank shall at least be 40 percent and gradually brought down to 26 percent within 12 years from the date of commencement of business of the bank.

- The foreign shareholding in the small finance bank would be as per the Foreign Direct Investment (FDI) policy for private sector banks as amended from time to time.

- The small finance banks will be required to extend 75 percent of their Adjusted Net Bank Credit (ANBC) to the sectors eligible for classification as priority sector lending (PSL) by the Reserve Bank.

- SFBs have to maintain the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) as per RBI norms.

- At least 50 percent of its loan portfolio should constitute loans and advances of up to Rs. 25 lakh.

What can SFBs do?

- Sell forex to customers.

- Sell mutual funds, insurance, and pensions.

- Can convert into a full-fledged bank.

What Small Finance Banks can’t do?

- Extend large loans.

- Cannot float subsidiaries and deal in sophisticated products.

Challenges to Small Finance Banks

- Have to compete with existing public sector banks and RRBs.

- Micro Finance Institutions (MFI)/NBFCs specialize in micro-lending operations with limited exposure to banking operations; which means they have to hire and train talent from the banking industry.

- The cost of deposit mobilization will be higher for these banks as they cover rural and underserved segments.

Payment Banks

- The objectives of setting up payment banks will be to further financial inclusion by providing (1) small savings accounts and (2) payments/remittance services to migrant labor workforce, low-income households, small businesses, other unorganized sector entities, and other users.

- They will not lend to customers and will have to deploy their funds in government papers and bank deposits.

Scope of activities

- Acceptance of demand deposits-Payments bank will initially be restricted to holding a maximum balance of Rs. 100,000 per individual customer.

- Issuance of ATM/debit cards-Payments banks, however, cannot issue credit cards.

- Payments and remittance services through various channels.

- Business Correspondents (BC) of another bank, subject to the Reserve Bank guidelines on BCs.

- Distribution of non-risk sharing simple financial products like mutual fund units and insurance products, etc.

- The payment bank cannot undertake lending activities.

Criteria for setting up Payment banks

- Existing non-bank Pre-paid Payment Instrument (PPI) issuers; and other entities such as individuals/professionals; Non-Banking Finance Companies (NBFCs), corporate Business Correspondents (BCs), mobile telephone companies, supermarket chains, companies, real sector cooperatives; that are owned and controlled by residents; and public sector entities may apply to set up payments banks.

- Promoter/promoter groups should be ‘fit and proper’ with a sound track record of professional experience or run their businesses for at least five years to be eligible to promote payment banks.

- The minimum paid-up equity capital for small finance banks shall be Rs. 100 crore.

- Maintains a minimum of 75% of deposits in Government bonds and a maximum of 25% deposits with other scheduled commercial banks.

- The promoter’s minimum initial contribution to the paid-up equity capital of such payments bank shall at least be 40 percent for the first five years from the commencement of its business.

- The bank should have a high-powered Customer Grievances Cell to handle customer complaints.

- The operations of the bank should be fully networked and technology-driven from the beginning, conforming to generally accepted standards and norms.

What can Payment Banks do?

- Offer internet banking, and sell mutual funds, insurance, and pensions.

- Have business correspondents and ATMs.

- Offer bill payment service for customers

- They can enable transfers and remittances from a mobile phone.

- They can offer forex services at charges lower than bank

- They can provide forex cards to travelers, usable as debit or ATM cards all over India.

- They can also offer card acceptance mechanisms to third parties such as “Apple Pay”.

What Payment Banks can’t do?

- Offer credit cards

- Extend loans

- Handle cross-border remittances

- Accept NRI deposits

Challenges for payment banks

- Low revenue can’t undertake any lending businesses and the income stream is initially restricted to charges on remittances and efficiency of operations.

- Required to invest a minimum of 75 percent of its “demand deposit balances” into government securities. This limits their ability to earn from the deposit base as well.

- Banks are already offering most services that payments banks can and hence, for payments banks to offer a new and differentiated proposition will not be easy.

- Other saving instruments like Kisan Vikas Patra, gold bonds, etc have better returns than payment banks.

- Experience from Jan Dhan Yojna has shown that many such no-frill accounts have remained dormant, thus affecting the viability of the banks.

Payment Banks vs Small Finance Banks

Image courtesy: Times of India

Newly Proposed Differentiated Banks

In addition to recently licensed differentiated banks such as payments banks and small finance banks, the Reserve Bank has been exploring the possibilities of licensing other differentiated banks such as custodian banks and banks concentrating on wholesale and long-term financing.

Custodian banks: Custodian Banks are specialized financial institutions mainly responsible for safeguarding a firm’s or individual’s financial assets and are typically not engaged in conventional retail lending.

Wholesale banks: Wholesale banks are lenders that cater to large corporates that require long-term finance, particularly those engaged in infrastructure development. Typically, these banks raise long-term funds which are exempted from maintaining regulatory requirements like cash reserve ratio and statutory liquidity ratio.

Summary and Way Forward

Image Courtesy: Business Standard

- Both Payments Banks and Small Finance Banks are ‘niche’ or ‘differentiated’ banks with the common objective of furthering financial inclusion.

- India’s domestic remittance market is estimated to be about Rs 800-900 billion and growing. With money transfers made possible through mobile phones, a big chunk of it, especially that of the migrant labor could shift to this new platform.

- Payment banks can also play a significant role in implementing the government Direct Benefit Transfer scheme, where subsidies on health care, education, and gas are paid directly to beneficiaries’ accounts.

- Payment banks have proved hugely popular in other developing countries. In Kenya, the most cited success story, Vodafone M-Pesa is used by two in three adults to store money, make purchases, and transfer funds to friends, relatives, etc.

Read: Paytm Payments Bank Debacle

Article by: Arun Kumar. Arun completed his B.Tech from Indian Institute of Technology (BHU), Varanasi. His interests include Economics and Current Affairs.

IAS/IPS/IFS Smart Preparation Strategy: FREE Mentorship – Register Now!

Aim IAS/IPS/IFS?

Excellent …work

Sir plz name those private sector entities which have returned their payment bank licence to the RBI in the Payment bank section….

Which is the first small finance bank to get licence

Nice article sir,

I have correction here,

Wholesale banks are excempt only from SLR. They have to maintain CRR with RBI.

Excellent article….

करता आपका कोइ शाखा बिहार राज्य मे है। यदि हां तो सुचित करें।

Correct it,

Payment banks recommend by Nachiket mor committee

Small financial banks recommend by usha Thorat committee.

This information is extremely outdated.